Best auto insurance rates are a top priority for most drivers, and finding the best deal can feel like a daunting task. Navigating the world of insurance policies, deductibles, and coverage options can be confusing, but understanding the key factors that influence your rates can make the process much smoother.

From your driving history and vehicle type to your location and credit score, several factors contribute to your insurance premiums. By understanding these factors and taking steps to improve your driving habits and vehicle maintenance, you can potentially lower your insurance costs. This guide provides a comprehensive overview of auto insurance rates, including how they’re determined, how to find the best deals, and how to maintain affordable coverage.

Understanding Auto Insurance Rates

Auto insurance rates are complex and can vary significantly from person to person. Understanding the factors that influence your rate can help you make informed decisions about your coverage and potentially save money.

Factors Affecting Auto Insurance Rates

Several factors contribute to your auto insurance rates. These factors can be broadly categorized into:

- Vehicle-related factors: These include the make, model, year, and safety features of your vehicle. For example, newer vehicles with advanced safety features typically have lower rates compared to older vehicles with fewer safety features.

- Driver-related factors: These include your age, driving history, credit score, and driving habits. Drivers with a clean driving record and good credit scores usually have lower rates.

- Location-related factors: These include your zip code, the density of the population, and the frequency of accidents in your area. Areas with higher crime rates or more traffic congestion may have higher rates.

- Coverage-related factors: These include the type and amount of coverage you choose, such as liability, collision, comprehensive, and uninsured motorist coverage. Higher coverage limits generally result in higher premiums.

Difference Between Base Rates and Individual Premiums

Your base rate is a starting point determined by your vehicle and location. It is a standard rate applied to all drivers in a particular area with the same vehicle. Your individual premium is calculated by adding your base rate to a series of factors specific to you, such as your driving history, credit score, and coverage choices.

Finding the best auto insurance rates can feel like a jungle, but taking the time to compare quotes and understand your coverage needs is essential. While you’re navigating those details, why not take a break and appreciate the beauty of nature?

Check out Exquisite House Plants Featuring Red and Green Leaves for some vibrant inspiration. Once you’ve refreshed your perspective, you’ll be ready to tackle those insurance quotes with renewed energy and find the best rates for your needs.

For example, a base rate for a 2020 Honda Civic in a particular zip code might be $100 per month. However, your individual premium could be higher or lower depending on your driving record, credit score, and coverage choices.

Impact of Driving Behaviors on Rates

Your driving behavior significantly impacts your insurance rates. Here are some examples:

- Traffic violations: Speeding tickets, reckless driving, and DUI convictions can increase your rates. The severity of the violation and the number of offenses will influence the impact on your premiums.

- Accidents: Accidents, even if you were not at fault, can increase your rates. The severity of the accident and the number of claims you have filed will affect the increase.

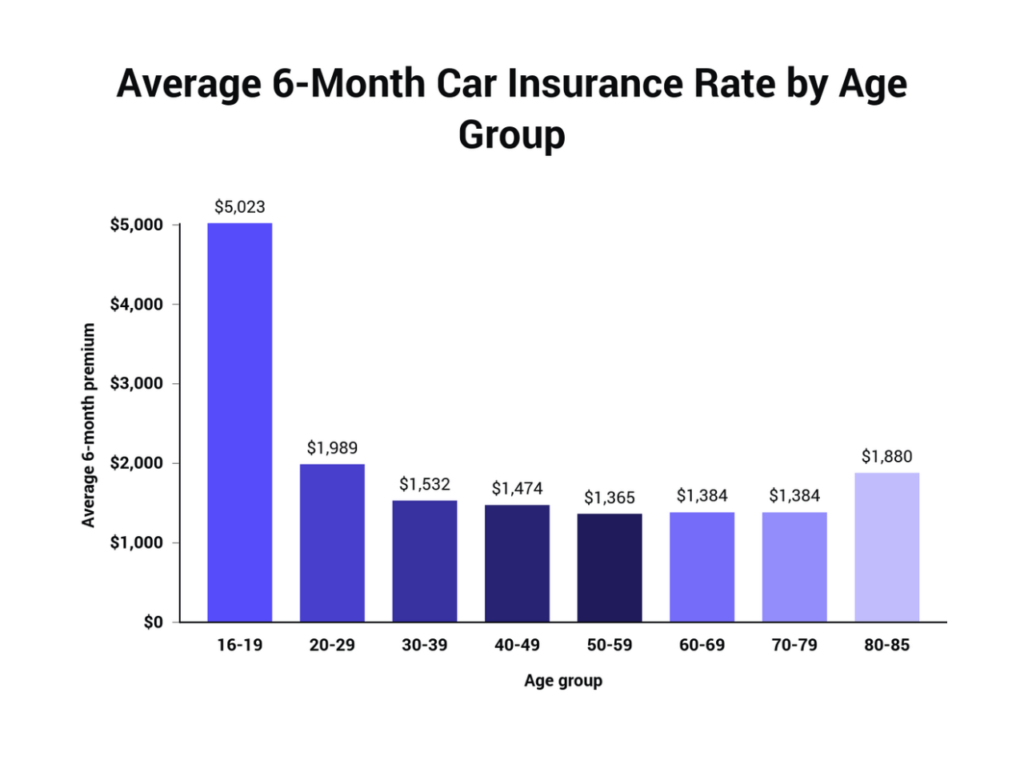

- Driving experience: New drivers typically have higher rates due to their lack of experience. As you gain experience and build a clean driving record, your rates may decrease.

Finding the Best Rates

Now that you understand how auto insurance rates are calculated, it’s time to put that knowledge to work and find the best possible rates for your needs. The key is to compare quotes from multiple insurers to ensure you’re getting the most competitive offer.

Comparing Quotes From Multiple Insurers

To find the best rates, it’s essential to get quotes from multiple insurers. This allows you to compare prices, coverage options, and other factors to make an informed decision. Here’s a step-by-step guide:

- Gather Your Information: Before you start requesting quotes, have your vehicle information readily available. This includes your vehicle identification number (VIN), make, model, year, and mileage. You’ll also need your driving history, including your driving record and any accidents or violations.

- Use Online Comparison Tools: Several websites allow you to compare quotes from multiple insurers simultaneously. These tools streamline the process and save you time. Popular options include:

- Compare.com: Compare.com is a popular platform for comparing quotes from various insurance providers.

- Policygenius: Policygenius is another comprehensive platform that allows you to compare quotes from top insurers.

- The Zebra: The Zebra is known for its user-friendly interface and comprehensive coverage options.

- Contact Insurers Directly: In addition to online comparison tools, you can contact insurers directly to get quotes. This allows you to discuss your specific needs and ask questions about their policies.

- Review Quotes Carefully: Once you have quotes from multiple insurers, carefully review each one. Pay attention to the coverage options, deductibles, premiums, and any discounts offered.

Comparing Key Features and Pricing

Here’s a table comparing key features and pricing of popular insurance companies:

| Company | Average Annual Premium | Discounts | Coverage Options | Customer Satisfaction |

|---|---|---|---|---|

| Geico | $1,428 | Good student, multi-car, defensive driving | Comprehensive, collision, liability, uninsured motorist | 4.5 out of 5 stars |

| Progressive | $1,500 | Safe driver, multi-policy, good student | Comprehensive, collision, liability, uninsured motorist | 4.0 out of 5 stars |

| State Farm | $1,600 | Safe driver, good student, multi-policy | Comprehensive, collision, liability, uninsured motorist | 4.2 out of 5 stars |

| Allstate | $1,700 | Safe driver, good student, multi-policy | Comprehensive, collision, liability, uninsured motorist | 3.8 out of 5 stars |

Note: These prices are estimates and may vary based on individual factors such as driving history, vehicle type, and location.

Evaluating Insurance Quotes

Once you have multiple quotes, it’s time to evaluate them and choose the best option. Here’s a checklist to help you make an informed decision:

- Coverage Options: Ensure the insurer offers the coverage you need, including liability, comprehensive, collision, and uninsured motorist coverage.

- Deductibles: Consider your risk tolerance and financial situation when choosing deductibles. Higher deductibles typically mean lower premiums, but you’ll pay more out of pocket if you have an accident.

- Premiums: Compare premiums from different insurers to find the most affordable option. Remember that the lowest price isn’t always the best option.

- Discounts: Check for available discounts, such as safe driver, good student, multi-car, and multi-policy discounts.

- Customer Service: Read reviews and ratings to assess the insurer’s customer service reputation.

- Financial Stability: Look for insurers with strong financial ratings, indicating their ability to pay claims in the event of an accident.

Insurance Coverage Options: Best Auto Insurance Rates

Understanding the various types of auto insurance coverage is crucial for making informed decisions about your policy. Different coverage options provide different levels of protection and come with varying costs. This section explores the common types of auto insurance coverage, their benefits, and their costs.

Liability Coverage

Liability coverage is the most basic type of auto insurance. It protects you financially if you cause an accident that injures another person or damages their property. Liability coverage typically includes two components:

- Bodily Injury Liability: This coverage pays for medical expenses, lost wages, and other damages resulting from injuries to other people in an accident you caused.

- Property Damage Liability: This coverage pays for repairs or replacement of damaged property, such as another vehicle or a building, that you are responsible for damaging.

Liability coverage limits are expressed as two numbers, such as 25/50/25. This means that the policy will pay up to $25,000 per person for bodily injury, up to $50,000 total for all bodily injury claims in a single accident, and up to $25,000 for property damage.

Liability coverage is legally required in most states, and the minimum limits vary. It’s essential to have enough liability coverage to protect yourself from significant financial losses.

Collision Coverage

Collision coverage pays for repairs or replacement of your vehicle if it’s damaged in an accident, regardless of who is at fault. If you’re in an accident with another vehicle and it’s your fault, liability coverage will pay for the other driver’s damages, but not yours. Collision coverage will cover your own vehicle’s repairs.

Collision coverage is optional, but it’s generally recommended if you have a car loan or lease. If you have an older vehicle with a low value, you might choose to forgo collision coverage and pay for repairs out of pocket if you have an accident.

Comprehensive Coverage

Comprehensive coverage protects your vehicle from damage caused by events other than accidents, such as theft, vandalism, fire, hail, or natural disasters. It also covers damage caused by animals, like deer or squirrels.

Comprehensive coverage is optional, but it’s a good idea to have it if you have a newer vehicle or a car with a high value. If your vehicle is older and has a lower value, you might choose to forgo comprehensive coverage and pay for repairs out of pocket if your car is damaged in a non-accident event.

Additional Considerations

While finding the best auto insurance rates often involves comparing quotes and choosing the right coverage, several other factors can significantly influence your premiums. Understanding these factors can help you make informed decisions and potentially save money on your insurance.

Credit History’s Impact

Your credit history plays a role in determining your auto insurance rates in many states. Insurance companies often use credit-based insurance scores (CBIS) to assess your risk. A good credit history generally translates to lower premiums, as it suggests you’re a responsible individual likely to make timely payments and avoid claims.

It’s important to note that not all states allow insurers to use credit history for pricing. Check your state’s regulations to see if this practice is permitted.

Geographic Location’s Influence, Best auto insurance rates

Your location can significantly affect your auto insurance rates. Insurance companies consider factors such as:

- Population density: Areas with high population density often have more traffic congestion and accidents, leading to higher premiums.

- Crime rates: Higher crime rates can increase the risk of theft or vandalism, which can affect insurance costs.

- Weather conditions: Regions prone to severe weather events like hurricanes, tornadoes, or hailstorms may have higher insurance premiums due to the increased risk of damage.

- Cost of repairs: Areas with higher costs of living generally have higher repair costs for vehicles, leading to higher insurance premiums.

Insurance Regulations and Consumer Protection

Insurance regulations and consumer protection laws vary by state. Understanding these regulations can help you:

- Identify unfair or discriminatory practices: Some states have laws prohibiting insurance companies from using certain factors, such as race or gender, to determine rates.

- Access consumer protection resources: Many states have insurance departments or consumer protection agencies that can help resolve disputes or provide information about your rights.

- Understand your rights: Knowing your rights as a consumer can empower you to challenge unfair practices or negotiate better rates.

Resources for Further Information

You may have questions about auto insurance that weren’t covered in this guide. Don’t worry; there are many resources available to help you get the information you need.

This section will explore reputable sources for information on auto insurance, including state insurance departments, consumer protection agencies, and organizations that offer assistance with insurance-related issues.

State Insurance Departments

State insurance departments are the primary regulators of the insurance industry in each state. They are responsible for licensing insurance companies, ensuring that they comply with state laws, and resolving consumer complaints.

Each state’s insurance department website provides valuable information on auto insurance, including:

- Consumer guides on auto insurance

- Information on required coverage and minimum limits

- Complaints procedures

- Lists of licensed insurance companies

- Information on fraud prevention

You can find your state’s insurance department website by searching online for “[your state] insurance department.”

Consumer Protection Agencies

Consumer protection agencies, such as the Federal Trade Commission (FTC) and the Consumer Financial Protection Bureau (CFPB), provide information and resources to consumers on a wide range of issues, including insurance.

These agencies can help you understand your rights as a consumer and resolve disputes with insurance companies.

The FTC and CFPB websites offer resources on auto insurance, including:

- Tips for choosing an insurance company

- Information on common insurance scams

- Guidelines for filing complaints

- Information on your rights under state and federal law

Organizations Offering Assistance

Several organizations offer assistance to consumers with insurance-related issues.

These organizations may provide free or low-cost services, such as:

- Insurance counseling

- Dispute resolution

- Consumer education

Here are some reputable organizations that offer assistance with insurance-related issues:

- The National Association of Insurance Commissioners (NAIC)

- The Insurance Information Institute (III)

- The National Consumer Law Center (NCLC)

- The Better Business Bureau (BBB)

These organizations can provide valuable information and support, especially if you are facing a difficult insurance situation.

End of Discussion

Finding the best auto insurance rates requires careful consideration of your individual needs and circumstances. By comparing quotes, understanding your coverage options, and taking advantage of discounts, you can find a policy that provides adequate protection at a price that fits your budget. Remember, insurance is an investment in your financial security, and it’s important to choose a policy that provides the right level of coverage for your specific situation.