Term life insurance cost is a crucial factor to consider when securing your family’s financial future. It’s a type of life insurance that provides coverage for a specific period, typically 10 to 30 years, and pays a death benefit to your beneficiaries if you pass away during that term. The cost of term life insurance varies greatly depending on several factors, including your age, health, lifestyle, and the amount of coverage you need. Understanding these factors and how they influence premiums is essential for making informed decisions about your life insurance needs.

This comprehensive guide will delve into the intricacies of term life insurance cost, exploring the factors that impact premiums, strategies for reducing costs, and tips for finding the best rates. We’ll also discuss the importance of comparing quotes from multiple insurers and understanding policy features and options. By the end of this guide, you’ll have a clear understanding of how to navigate the world of term life insurance and find the most cost-effective solution for your unique circumstances.

Understanding Term Life Insurance: Term Life Insurance Cost

Term life insurance is a type of life insurance that provides coverage for a specific period, known as the term. It is a simple and affordable way to protect your loved ones financially in case of your death during the term.

Key Features and Benefits of Term Life Insurance

Term life insurance is designed to provide financial protection for a specific period, typically 10, 20, or 30 years. It offers several benefits, making it an attractive option for many individuals and families:

- Affordability: Term life insurance is generally more affordable than permanent life insurance, such as whole life or universal life. This is because it only provides coverage for a limited period, and premiums are calculated based on the term length and your age.

- Simplicity: Term life insurance policies are typically straightforward and easy to understand. They focus on providing a death benefit during the policy term, without complex investment features or cash value accumulation.

- Flexibility: You can choose a term length that suits your needs, allowing you to tailor the coverage to your specific financial goals and circumstances. For example, you might choose a 20-year term if you have young children and want to ensure their financial security until they reach adulthood.

- Financial Protection: In the event of your death during the term, your beneficiaries will receive a lump-sum death benefit. This can help them cover expenses such as funeral costs, mortgage payments, outstanding debts, and provide financial stability for their future.

Term Life Insurance vs. Other Types of Life Insurance

Term life insurance is often compared to permanent life insurance, such as whole life or universal life. While both types of life insurance provide a death benefit, there are key differences:

| Feature | Term Life Insurance | Permanent Life Insurance |

|---|---|---|

| Coverage Period | Specific term (e.g., 10, 20, 30 years) | Lifetime coverage |

| Premiums | Generally lower and fixed for the term | Higher and may increase over time |

| Cash Value | No cash value accumulation | Cash value component that grows over time |

| Investment Features | No investment features | May offer investment options |

Term life insurance is a cost-effective way to provide financial protection for a specific period, while permanent life insurance offers lifetime coverage and cash value accumulation. The best type of life insurance for you will depend on your individual needs and financial goals.

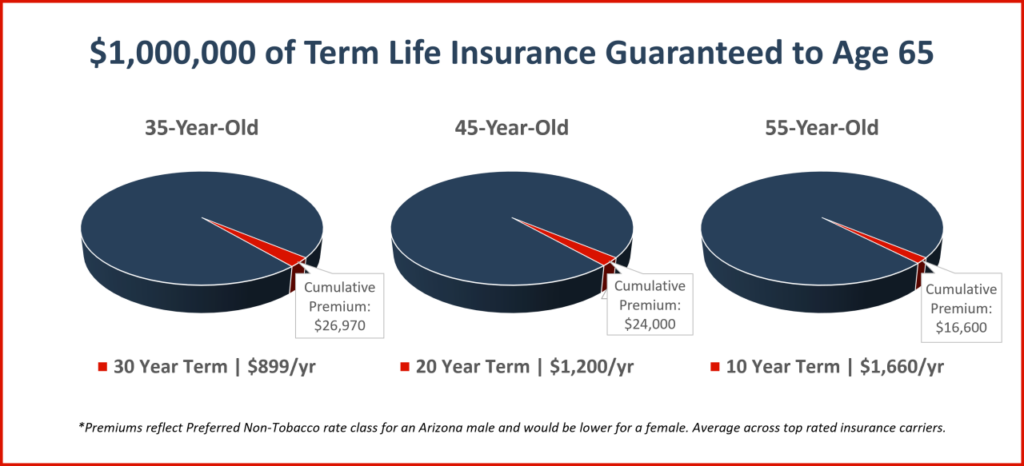

Factors Influencing Term Life Insurance Cost

The cost of term life insurance is determined by several factors. These factors are carefully considered by insurance companies to assess the risk associated with insuring your life. Understanding these factors can help you make informed decisions about your coverage and ensure you get the best value for your premium.

Age

Your age is a significant factor in determining your term life insurance premium. As you get older, your risk of death increases, leading to higher premiums. This is because life expectancy decreases with age, and insurance companies need to account for this increased risk. For example, a 30-year-old individual will typically pay a lower premium than a 50-year-old individual for the same coverage amount.

Health, Term life insurance cost

Your health plays a crucial role in determining your term life insurance cost. Individuals with pre-existing medical conditions, such as diabetes, heart disease, or cancer, are considered higher risk. This is because they are more likely to develop health complications and die prematurely. Insurance companies may charge higher premiums or even deny coverage to individuals with certain health conditions.

Lifestyle

Your lifestyle choices, such as smoking, alcohol consumption, and risky hobbies, can impact your term life insurance premium. Smoking is a major risk factor for several health issues, including lung cancer and heart disease. Individuals who smoke are generally charged higher premiums than non-smokers. Similarly, engaging in risky activities like skydiving or mountain climbing can increase your risk of death and result in higher premiums.

Coverage Amount

The amount of coverage you choose will also affect your premium. The higher the coverage amount, the more you will pay. This is because you are essentially insuring a larger sum of money, and the insurance company needs to charge a higher premium to cover the increased risk. It’s essential to choose a coverage amount that meets your financial needs while considering your budget.

Smoking

Smoking is a significant factor that can significantly increase your term life insurance premium. Insurance companies consider smokers to be at a higher risk of developing health problems, such as lung cancer, heart disease, and stroke. This increased risk translates into higher premiums for smokers.

The average smoker pays about 50% more for term life insurance than a non-smoker.

Pre-Existing Conditions

If you have a pre-existing medical condition, you may be charged a higher premium for term life insurance. This is because individuals with pre-existing conditions are considered higher risk due to their increased likelihood of developing health complications and dying prematurely.

For example, individuals with diabetes, heart disease, or cancer may be charged higher premiums or even denied coverage.

Risky Hobbies

Engaging in risky hobbies, such as skydiving, mountain climbing, or scuba diving, can also impact your term life insurance premium. These activities increase your risk of death or injury, which translates into higher premiums for insurance companies.

If you engage in risky hobbies, you may be required to disclose this information to the insurance company, which could result in higher premiums or even denial of coverage.

Ultimate Conclusion

Ultimately, choosing the right term life insurance policy comes down to finding the right balance between affordability and coverage. By understanding the factors that influence premiums, comparing quotes from multiple insurers, and carefully reviewing policy terms, you can ensure that you’re getting the most value for your money. Remember, term life insurance is a vital tool for protecting your loved ones and securing their financial well-being. By making informed decisions and taking proactive steps, you can create a solid financial foundation for your family’s future.

The cost of term life insurance can vary greatly depending on factors like age, health, and coverage amount. One popular provider to consider is nationwide life insurance , which offers a range of options to suit different needs. Getting quotes from multiple insurers and comparing rates is always a good idea to ensure you’re getting the best value for your term life insurance coverage.